“Per new compliance rules, please use the attached form and send today. Our new IBAN is included.”

The logo looks correct. The tone is professional. The file is a neat PDF.

Aisha replies, “Received.” She schedules the transfer for USD 78,500.

Five minutes later, your sales manager pings: “Supplier says payment is overdue. Did we pay?”

Aisha answers confidently, “Yes—just sent.”

The supplier replies, “We didn’t receive anything. Also, we never changed our bank.”

Your stomach drops.

That is Business Email Compromise (BEC)—not ransomware, not a virus pop-up, just convincing fraud using email and timing. It happens fast and, without preparation, the money is gone.

Let’s make sure it never happens to you.

What is BEC (in plain English)?

Business Email Compromise is when criminals trick your team into sending money or data by pretending to be a trusted person—like your supplier, CFO, CEO, or payroll provider. It often involves:

Invoice / vendor fraud: “Here are our new bank details.”

CEO/CFO fraud: “Process this urgent payment; I’m boarding a flight.”

Payroll rerouting: “Please change my salary account.”

Account takeover: Criminals log into a real mailbox and reply inside the thread.

There may be no malware, no attachment, no obvious signs—just credibility, speed, and pressure.

Mule account — Money is sent to a local/foreign account and then disappears.

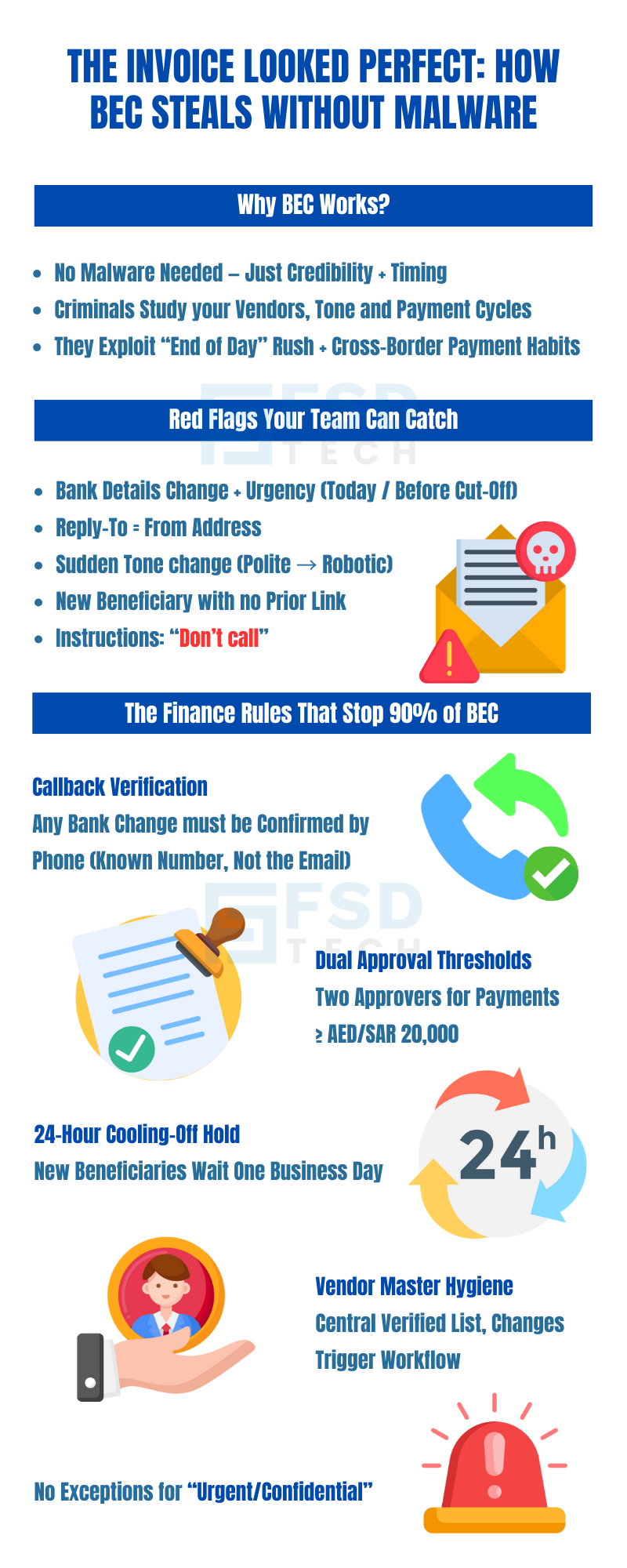

Red flags your team can spot

Bank change + urgency (today, end-of-day, before cut-off).

Reply-to mismatch (From says one domain; Reply-To is different).

Tone change (a normally polite contact sounds robotic or pushy).

New beneficiaries without a prior relationship.

Attachments with instructions to avoid calling anyone.

If a vendor’s account number changes, finance must call a known phone number on file (or independently verified) before paying. Never call a number listed in the email requesting the change.

Any payment ≥ your risk threshold (e.g., USD 5,000 / SAR 20,000 / AED 20,000) requires two approvers from different departments.

For first-time or changed accounts, schedule the payment for next business day unless a call-back verification clears it.

Keep a verified vendor master list (official emails, phone, bank). Only AP can edit; changes generate an approval workflow.

A CEO can fast-track—but only by following the same callback rule via a known number or in-person confirmation.

Rule of thumb: If the money flow or banking details change, the communication channel must change too (email → phone call to a known number, never the number in the email).

The 3-Layer Technical Safety Net (that doesn’t slow business)

1) Zero Dwell Containment (Xcitium)

If a PDF or form is malicious, Zero Dwell opens it in a safe bubble first. Unknown files can’t harm devices or steal session cookies—even if someone clicks. It’s instant, invisible to users, and critical when invoices and “forms” are flying around.

2) EDR (Endpoint Detection & Response)

EDR watches endpoints for weird behavior—like scripts that try to access email tokens, mass-forward mail, or plant persistence. It can block suspicious actions and gives your team a timeline of what happened.

3) MDR (Managed Detection & Response)

When minutes matter, a human SOC team validates alerts 24/7, isolates devices, hunts for mailbox rules, and acts now—not tomorrow morning.

Together: Zero Dwell stops the booby-trapped document, EDR catches abnormal behavior, MDR ensures a swift response if anything slips through.

The finance side: simple process controls that defeat BEC

You don’t need an army of auditors. You need five practical rules:

Out-of-band verification for bank changes

Dual approval thresholds

24-hour “cooling-off” hold for new beneficiaries

Vendor master hygiene

No “urgent confidential” exceptions

These five rules stop 90%+ of BEC attempts—because the criminal’s plan relies on email-only instructions.

Revoke tokens and reset app passwords (IMAP/POP if used).

Contact law enforcement (jurisdiction-specific) and your bank’s fraud team for trace actions.

Prepare communications: Clear message to staff (“what to look for”), to supplier (“we’re handling; please do not accept bank change requests by email without a callback”), and to impacted customers if needed.

Day 1–3

Strengthen identity: Enforce MFA for all mailboxes; disable legacy protocols (IMAP/POP) where possible; restrict external auto-forwarding.

Email authentication: Ensure SPF/DKIM/DMARC are configured; raise DMARC policy over time (monitor → quarantine → reject).

Finance policy refresh: Train AP/AR on the 5 rules; post the callback script by every desk.

Post-incident review: What worked, what was slow, and who needs shortcuts fixed (e.g., faster vendor verification).

Practical scripts your team can use

Callback script (bank change verification)

“Hi [Vendor Name], this is [Your Name] from [Company]. We received an email requesting a bank account change for future payments. We are calling the number on our existing vendor record to confirm.

1) Did you request a change?

2) What is the old account number ending with…?

3) What is the new account number and bank name?

We will update our system after this call and send a confirmation email.”

Staff announcement (slack/teams/email)

“Team: All bank account changes, payment method changes, and urgent payment requests must be verified by a phone call to a known number. Email alone is not enough. If you’re unsure, pause and ask Finance. No one will be penalized for delaying a suspicious request.”

Vendor email (post-incident)

“We are improving our payment security. From now on, any banking changes must be confirmed by a phone call to the number we already have on file. We will not accept changes confirmed by email or chat alone.”

Monthly executive report: clear metrics, incidents, and next steps—no jargon.

Final word

BEC doesn’t shout. It whispers “urgent” and “routine” at the same time.

You don’t beat it with fear—you beat it with simple rules and quiet, always-on safety nets:

Change in money flow? Change the channel. (Email → phone call)

Two approvals, one cool-off day.

Zero Dwell + EDR + MDR to catch the tricks and respond fast.

Book a quick strategy call with our experts to see how to apply these controls in your company. Book Now

FAQ

1) What is Business Email Compromise (BEC)?

Business Email Compromise (BEC) is a cybercrime where criminals trick your company into sending money or sensitive information by pretending to be someone you trust—like your CEO, CFO, supplier, or payroll provider. They often send emails that look completely genuine, sometimes even from real compromised accounts. BEC scams don’t always involve malware; they rely on social engineering—manipulating people’s trust to achieve their goals.

2) How is BEC different from regular phishing?

Phishing usually casts a wide net—hundreds or thousands of emails hoping someone clicks. BEC is highly targeted. Criminals research your business, know your payment habits, and time their emails to seem normal. While phishing often tries to steal login details, BEC’s main goal is to direct money transfers or gain access to valuable data.

3) What is invoice fraud?

Invoice fraud is a type of BEC where a scammer sends a fake invoice or changes the bank details on a real invoice. The goal is to get you to pay the money into the criminal’s account instead of the real supplier’s. Because invoices are common and expected in business, this method often goes unnoticed until it’s too late.

4) Why is BEC common in GCC & Africa?

Several factors make the region a target:

Frequent cross-border payments with changing bank details.

High use of email and WhatsApp for business communications.

Businesses operating in multiple languages, increasing miscommunication risk.

SMBs without formal finance controls (e.g., no dual approval or callback verification).

5) How do criminals get access to our emails?

They use several methods:

Phishing for credentials (fake login pages).

Buying leaked passwords from the dark web.

Guessing weak passwords (like companyname@123).

Infecting devices with malware that steals email session tokens. Once inside, they may set up auto-forwarding rules to spy on conversations without you knowing.

6) What are the red flags of BEC or invoice fraud?

Urgent requests for payment changes.

Bank account changes that seem sudden or unusual.

“Reply-To” address different from the “From” address.

Unusual language or tone changes in emails.

Instructions not to confirm by phone or in person.

7) What is the callback verification rule?

It’s a simple but powerful safeguard: If payment details change, confirm it through a different communication channel. That means calling a known number (from your vendor master file, not the email) to verify before making the change. This one step can stop most invoice fraud attempts.

8) How can Zero Dwell Containment help prevent BEC?

If a malicious invoice or payment form arrives, Zero Dwell opens it in a safe, isolated environment—instantly—before it can interact with your system. This stops any embedded malware from stealing your email login or installing spyware, even if someone opens the file.

9) How does EDR help in BEC cases?

Answer:

EDR (Endpoint Detection & Response) monitors computers and devices for suspicious behavior—like creating hidden email rules, logging in from unusual locations, or running scripts from invoice attachments. It blocks harmful actions and alerts your IT team for investigation.

10) Why is MDR important for SMBs facing BEC?

MDR (Managed Detection & Response) gives you 24/7 human security experts who can act immediately—isolating compromised devices, shutting down suspicious sessions, and removing malicious mailbox rules—even outside business hours. SMBs benefit because they don’t have to hire a full in-house security team.

11) What are the finance process changes that can stop BEC?

Dual approval for payments above a set amount.

Mandatory callback verification for bank changes.

24-hour waiting period for new beneficiaries.

Vendor master list with verified contacts.

No exceptions for “urgent confidential” payment requests.

12) Can BEC happen without malware?

Yes. Many BEC cases involve no malware at all—just a convincing email. That’s why it’s important to focus on human verification processes as well as technical defenses.

13) What should we do if we think we’ve been hit by BEC?

Call your bank immediately to freeze the transfer.

Contact the receiving bank’s fraud team.

Isolate affected devices and reset passwords.

Remove suspicious email forwarding rules.

Inform your supplier and any impacted parties.

Notify your security team or MDR provider.

14) How much can BEC cost a small business?

Losses vary but can range from a few thousand dollars to hundreds of thousands—sometimes more than the company’s annual profit. The damage isn’t just financial; it also hits trust, relationships, and sometimes legal compliance.

15) How fast can FSD-Tech protect us against BEC?

Deployment is quick: Zero Dwell Containment and EDR can be installed within a day, and MDR monitoring starts immediately after setup. Finance process training can be completed in a week, ensuring both technical and human safeguards are in place fast.

About The Author

Anas Abdu Rauf

Anas is an Expert in Network and Security Infrastructure, With over seven years of industry experience, holding certifications Including CCIE- Enterprise, PCNSE, Cato SASE Expert, and Atera Certified Master. Anas provides his valuable insights and expertise to readers.

.webp&w=3840&q=75)

.webp&w=3840&q=75)

share your thoughts